R Provider Tutorial

Referencing the provider

In order to use the R provider, you need to reference the RDotNet.dll library

(which is a .NET connector for R) and the RProvider.dll itself. For this tutorial,

we use open to reference a number of packages including stats, tseries and zoo:

1: 2: 3: 4: 5: 6: 7: 8: 9: 10: 11: 12: 13: 14: 15: 16: |

|

If either of the namespaces above are unrecognized, you need to install the package in R

using install.packages("stats").

Obtaining data

In this tutorial, we use F# Data to access stock prices from the Yahoo Finance portal. For more information, see the documentation for the CSV type provider.

The following snippet uses the CSV type provider to generate a type Stocks that can be

used for parsing CSV data from Yahoo. Then it defines a function getStockPrices that returns

array with prices for the specified stock and a specified number of days:

1: 2: 3: 4: 5: 6: 7: 8: 9: 10: 11: 12: 13: 14: |

|

Calling R functions

Now, we're ready to call R functions using the type provider. The following snippet takes

msftOpens, calculates logarithm of the values using R.log and then calculates the

differences of the resulting vector using R.diff:

1: 2: |

|

If you want to see the resulting values, you can call msft.AsVector() in F# Interactive.

Next, we use the acf function to display the atuo-correlation and call adf_test to

see if the msft returns are stationary/non-unit root:

1: 2: |

|

After running the first snippet, a window similar to the following should appear (note that it might not appear as a top-most window).

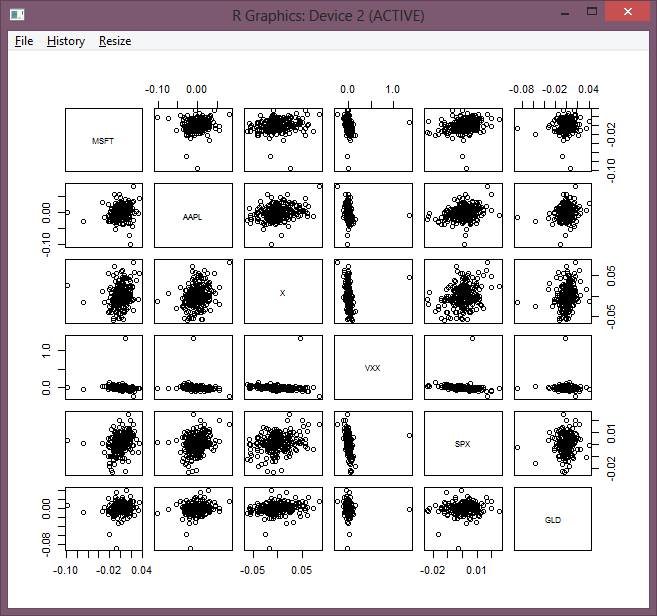

Finally, we can obtain data for multiple different indicators and use the R.pairs function

to produce a matrix of scatter plots:

1: 2: 3: 4: 5: 6: 7: 8: 9: 10: 11: |

|

As a result, you should see a window showing results similar to these:

Full name: Tutorial.Stocks

Full name: FSharp.Data.CsvProvider

<summary>Typed representation of a CSV file.</summary>

<param name='Sample'>Location of a CSV sample file or a string containing a sample CSV document.</param>

<param name='Separators'>Column delimiter(s). Defaults to `,`.</param>

<param name='InferRows'>Number of rows to use for inference. Defaults to `1000`. If this is zero, all rows are used.</param>

<param name='Schema'>Optional column types, in a comma separated list. Valid types are `int`, `int64`, `bool`, `float`, `decimal`, `date`, `guid`, `string`, `int?`, `int64?`, `bool?`, `float?`, `decimal?`, `date?`, `guid?`, `int option`, `int64 option`, `bool option`, `float option`, `decimal option`, `date option`, `guid option` and `string option`.

You can also specify a unit and the name of the column like this: `Name (type<unit>)`, or you can override only the name. If you don't want to specify all the columns, you can reference the columns by name like this: `ColumnName=type`.</param>

<param name='HasHeaders'>Whether the sample contains the names of the columns as its first line.</param>

<param name='IgnoreErrors'>Whether to ignore rows that have the wrong number of columns or which can't be parsed using the inferred or specified schema. Otherwise an exception is thrown when these rows are encountered.</param>

<param name='SkipRows'>SKips the first n rows of the CSV file.</param>

<param name='AssumeMissingValues'>When set to true, the type provider will assume all columns can have missing values, even if in the provided sample all values are present. Defaults to false.</param>

<param name='PreferOptionals'>When set to true, inference will prefer to use the option type instead of nullable types, `double.NaN` or `""` for missing values. Defaults to false.</param>

<param name='Quote'>The quotation mark (for surrounding values containing the delimiter). Defaults to `"`.</param>

<param name='MissingValues'>The set of strings recogized as missing values. Defaults to `NaN,NA,N/A,#N/A,:,-,TBA,TBD`.</param>

<param name='CacheRows'>Whether the rows should be caches so they can be iterated multiple times. Defaults to true. Disable for large datasets.</param>

<param name='Culture'>The culture used for parsing numbers and dates. Defaults to the invariant culture.</param>

<param name='Encoding'>The encoding used to read the sample. You can specify either the character set name or the codepage number. Defaults to UTF8 for files, and to ISO-8859-1 the for HTTP requests, unless `charset` is specified in the `Content-Type` response header.</param>

<param name='ResolutionFolder'>A directory that is used when resolving relative file references (at design time and in hosted execution).</param>

<param name='EmbeddedResource'>When specified, the type provider first attempts to load the sample from the specified resource

(e.g. 'MyCompany.MyAssembly, resource_name.csv'). This is useful when exposing types generated by the type provider.</param>

Full name: Tutorial.getStockPrices

Returns prices of a given stock for a specified number

of days (starting from the most recent)

val float : value:'T -> float (requires member op_Explicit)

Full name: Microsoft.FSharp.Core.Operators.float

--------------------

type float = Double

Full name: Microsoft.FSharp.Core.float

--------------------

type float<'Measure> = float

Full name: Microsoft.FSharp.Core.float<_>

member Clone : unit -> obj

member CopyTo : array:Array * index:int -> unit + 1 overload

member GetEnumerator : unit -> IEnumerator

member GetLength : dimension:int -> int

member GetLongLength : dimension:int -> int64

member GetLowerBound : dimension:int -> int

member GetUpperBound : dimension:int -> int

member GetValue : params indices:int[] -> obj + 7 overloads

member Initialize : unit -> unit

member IsFixedSize : bool

...

Full name: System.Array

Full name: Microsoft.FSharp.Collections.Array.rev

Full name: Tutorial.msftOpens

Get opening prices for MSFT for the last 255 days

Full name: Tutorial.msft

static member ! : ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member != : ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member !_hexmode : ?a: obj -> SymbolicExpression + 1 overload

static member !_octmode : ?a: obj -> SymbolicExpression + 1 overload

static member $ : ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member $<- : ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member $<-_data_frame : ?x: obj * ?name: obj * ?value: obj -> SymbolicExpression + 1 overload

static member $_DLLInfo : ?x: obj * ?name: obj -> SymbolicExpression + 1 overload

static member $_data_frame : ?x: obj * ?name: obj -> SymbolicExpression + 1 overload

static member $_package__version : ?x: obj * ?name: obj -> SymbolicExpression + 1 overload

...

Full name: RProvider.R

Base R functions.

R.log(?paramArray: obj []) : SymbolicExpression

Logarithms and Exponentials

R.diff(?x: obj, ?___: obj, ?paramArray: obj []) : SymbolicExpression

Lagged Differences

Full name: Tutorial.a

static member AIC : ?object: obj * ?___: obj * ?k: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member ARMAacf : ?ar: obj * ?ma: obj * ?lag_max: obj * ?pacf: obj -> SymbolicExpression + 1 overload

static member ARMAtoMA : ?ar: obj * ?ma: obj * ?lag_max: obj -> SymbolicExpression + 1 overload

static member BIC : ?object: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member Box_test : ?x: obj * ?lag: obj * ?type: obj * ?fitdf: obj -> SymbolicExpression + 1 overload

static member C : ?object: obj * ?contr: obj * ?how_many: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member D : ?expr: obj * ?name: obj -> SymbolicExpression + 1 overload

static member Gamma : ?link: obj -> SymbolicExpression + 1 overload

static member HoltWinters : ?x: obj * ?alpha: obj * ?beta: obj * ?gamma: obj * ?seasonal: obj * ?start_periods: obj * ?l_start: obj * ?b_start: obj * ?s_start: obj * ?optim_start: obj * ?optim_control: obj -> SymbolicExpression + 1 overload

static member IQR : ?x: obj * ?na_rm: obj * ?type: obj -> SymbolicExpression + 1 overload

...

Full name: RProvider.stats.R

R statistical functions.

R.acf(?x: obj, ?lag_max: obj, ?type: obj, ?plot: obj, ?na_action: obj, ?demean: obj, ?___: obj, ?paramArray: obj []) : SymbolicExpression

Auto- and Cross- Covariance and -Correlation Function Estimation

Full name: Tutorial.adf

static member MATCH : ?x: obj * ?table: obj * ?nomatch: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member MATCH_default : ?x: obj * ?table: obj * ?nomatch: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member MATCH_times : ?x: obj * ?table: obj * ?nomatch: obj * ?units: obj * ?eps: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member ORDER : ?x: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member ORDER_default : ?x: obj * ?___: obj * ?na_last: obj * ?decreasing: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member Sys_yearmon : ?NULL: obj -> SymbolicExpression + 1 overload

static member Sys_yearqtr : ?NULL: obj -> SymbolicExpression + 1 overload

static member as_Date : ?x: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member as_Date_numeric : ?x: obj * ?origin: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member as_Date_ts : ?x: obj * ?offset: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

...

Full name: RProvider.zoo.R

An S3 class with methods for totally ordered indexed

observations. It is particularly aimed at irregular time series

of numeric vectors/matrices and factors. zoo's key design goals

are independence of a particular index/date/time class and

consistency with ts and base R by providing methods to extend

standard generics.

Full name: Tutorial.tickers

Full name: Tutorial.data

Full name: Microsoft.FSharp.Core.ExtraTopLevelOperators.printfn

Full name: Tutorial.df

R.data_frame(?___: obj, ?row_names: obj, ?check_rows: obj, ?check_names: obj, ?stringsAsFactors: obj, ?paramArray: obj []) : SymbolicExpression

Data Frames

Full name: RProvider.Helpers.namedParams

static member Axis : ?x: obj * ?at: obj * ?___: obj * ?side: obj * ?labels: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member abline : ?a: obj * ?b: obj * ?h: obj * ?v: obj * ?reg: obj * ?coef: obj * ?untf: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member arrows : ?x0: obj * ?y0: obj * ?x1: obj * ?y1: obj * ?length: obj * ?angle: obj * ?code: obj * ?col: obj * ?lty: obj * ?lwd: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member assocplot : ?x: obj * ?col: obj * ?space: obj * ?main: obj * ?xlab: obj * ?ylab: obj -> SymbolicExpression + 1 overload

static member axTicks : ?side: obj * ?axp: obj * ?usr: obj * ?log: obj * ?nintLog: obj -> SymbolicExpression + 1 overload

static member axis : ?side: obj * ?at: obj * ?labels: obj * ?tick: obj * ?line: obj * ?pos: obj * ?outer: obj * ?font: obj * ?lty: obj * ?lwd: obj * ?lwd_ticks: obj * ?col: obj * ?col_ticks: obj * ?hadj: obj * ?padj: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member axis_Date : ?side: obj * ?x: obj * ?at: obj * ?format: obj * ?labels: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member axis_POSIXct : ?side: obj * ?x: obj * ?at: obj * ?format: obj * ?labels: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member barplot : ?height: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

static member barplot_default : ?height: obj * ?width: obj * ?space: obj * ?names_arg: obj * ?legend_text: obj * ?beside: obj * ?horiz: obj * ?density: obj * ?angle: obj * ?col: obj * ?border: obj * ?main: obj * ?sub: obj * ?xlab: obj * ?ylab: obj * ?xlim: obj * ?ylim: obj * ?xpd: obj * ?log: obj * ?axes: obj * ?axisnames: obj * ?cex_axis: obj * ?cex_names: obj * ?inside: obj * ?plot: obj * ?axis_lty: obj * ?offset: obj * ?add: obj * ?args_legend: obj * ?___: obj * ?paramArray: obj [] -> SymbolicExpression + 1 overload

...

Full name: RProvider.graphics.R

R functions for base graphics.

R.pairs(?x: obj, ?___: obj, ?paramArray: obj []) : SymbolicExpression

Scatterplot Matrices